Amanah Saham Nasional Berhad (ASNB) recently announced income distribution and bonus for their largest inhouse fund, Amanah Saham Bumiputra (ASB). With 8.87 million unit holders invested into ASB, the annual income and bonus announcement is an eagerly anticipated event each year. Fortunately for 2015, ASB did not disappoint by posting an income distribution of 7.25 cents per unit and a bonus of 0.50 cents per unit for Financial Year End 31st December 2015.

However looking at the latest income distribution and bonus from ASB, I observed a few problems with ASB that should be highlighted to the masses. I'm putting up this post not to spread fear or panic. Instead I am trying to highlight my personal observations with regards to the possible risk that ASB investors could face in the near future. I might be right or I could be wrong. Ultimately you as an investor should make your own judgement call.

Let's begin then....

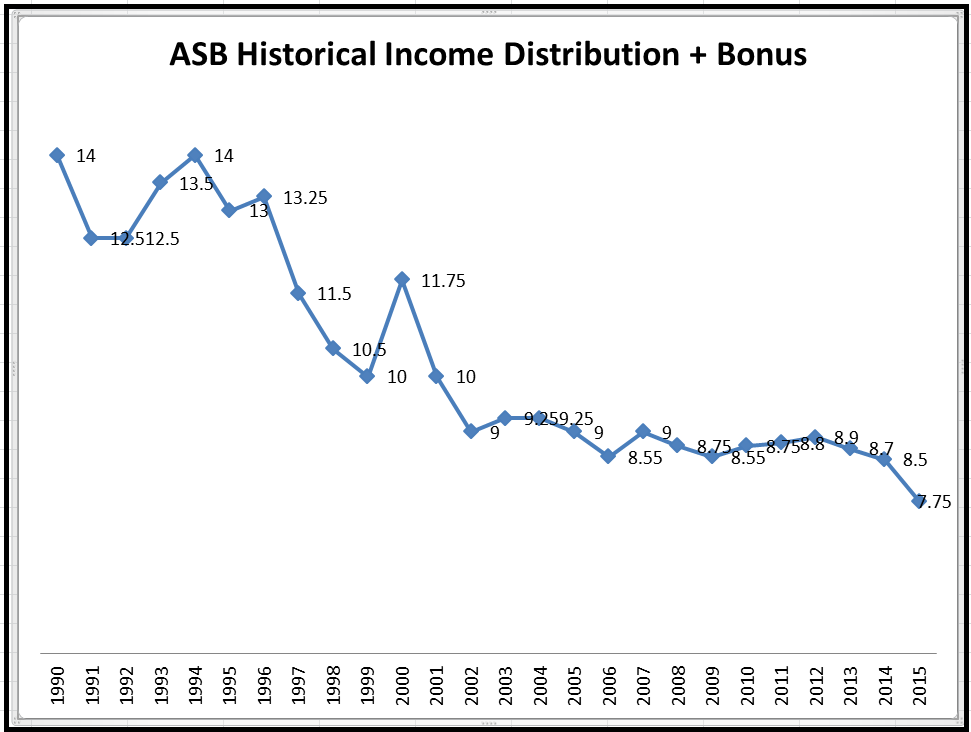

Did you know that ASB's income distribution and bonus has been on a downtrend since 1990!

Take a look at this graph of ASB historical income distribution + bonus from 1990 till 2015:

|

ASB historical income distribution + bonus from 1990 till 2015

|

Judging from the graphical trend, investors should expect ASB income distribution and bonus to head even further south in the near future. Results from Financial Year End 2015 already gave the first warning sign. Simple because 2015's ASB income distribution + bonus fell below the 8% reference mark for the very first time!

If you're not aware, the 8% return is the general benchmark value used by many when referring to ASB's annual returns. 8% is used to calculate and project gains when one intends to take up a long term personal loan to invest into ASB. The 8% is also used by many to calculate future projection of ASB returns.

With this key figure being breached for the first time in history, I believe a feeling of uncertainty is slowing emerging among many ASB investors. How much further will future distributions and bonus fall? What if the income distribution and bonus falls drops below the interest rate of the personal loan taken up by ASB investors?

What's causing the falling income distribution and bonus? I believe there's two main reason for the decline in ASB's income distribution and bonus.

Reason 1 : ASB is just too big!

Based on the latest statistics (31 Dec 2015), ASB itself is managing RM142.54 billion worth of investments for 8.87million investors. That approximately 25% of our EPF fund size!

Take a look at the growth of ASB's fund size below:

- 2012 - RM110.298 billion

- 2013 - RM127.393 billion

- 2014 - RM137.373 billion

- 2015 - RM142.540 billion

Within a short period of 3 years, ASB has added an astounding RM32 billion to its size! If it wasn't for the launching of ASB2 in April 2014, ASB would have grown substantially bigger by now. If you like to read more about ASB2, check out this post from CompareHero.my

|

| ASB2 was launched to reduce the burden of ASB |

With an ever growing fund size, the biggest challenge for ASB is to generate a decent income distribution + bonus. Just take a look at the history of gross income (2012-2014) for ASB as shown in the table below:

|

| 2012-2014 ASB Total Gross Income |

Despite the rise in gross income between 2012 to 2014 (see the red box), income distribution + bonus continues to drop from 2012 to 2014 (from 8.9% to 8.7% to 8.5%). In other words, ASB's fund size is growing faster than the growth rate of its annual gross income.

What's more worrying is the fact that for 2015, ASB total gross income is decreasing as compared to the previous year. As of 23 Dec 2015, ASB recorded a total gross income off RM10.06 billion, approximately RM700+ million lesser than 2014's gross income. Now do you see the reason for the drop in income distribution + bonus for 2015?

Reason 2 : ASB is invested only into local equity

As stated in Reason 1, ASB is like a very big fish in a small pond (Malaysia equity market). This big fish is growing at an astounding rate yet there's simply not enough food in that small little pond to feed the hungry appetite of this fish.

This simple analogy is the perfect description of the situation that ASB is currently facing. With RM140+ billion in managed fund (and growing), there not much room to make decent returns if they are to continue investing only in local Malaysian equities.

What about the other "big fish" in the pond? Won't EPF be facing the same problem as well?

With RM600+ billion in managed funds, EPF knew many years ago that the only way to grow is to expand overseas. Through their Strategic Asset Allocation policy, EPF has started to expand overseas whereby in 2014 itself, 24% of EPF managed fund are parked abroad. This strategy proved to be a success when EPF announced an outstanding dividend distribution of 6.75% for 2014! For 2015 it is expected that EPF will be announcing a higher dividend, largely due to the increased profits from their overseas investments.

Will ASB follow the footsteps of EPF?

I believe the answer is NO. I've checked ASB's Product Highlight Sheet and find that there is no specific mention about investing into overseas equities. I've also checked the Investment Strategy section of ASB's 2014 Annual Report (refer to Page 15 of ASB 2014 Annual Report) only to find the same outcome. In a nutshell, if ASB does not expand their investment overseas, things might not be so rosy for ASB investors in the years to come.

Summary

In the past, all you need to do is just park your savings with ASB. Fill up the RM200,000 per individual quota as well as the RM50,000 per children quota and let ASB high income distribution and bonus do its own compounding wonders. When the time comes, you can retire comfortably.

Can this methodology of passive investing still work? Would you continue to park all your eggs in a single basket (ASB) now that the basket is showing signs of weakness?

With all the figures about ASB laid before your eyes plus the possibility of lower income and bonus distribution in the future, what would your next course of action be? Are you going to close an eye and hope for the best? Or perhaps it is time that you start looking for alternatives? How about Sukuks? Or Unit Trust? REITS maybe? Or just leave your money with EPF instead?

Since I write intensively on unit trust investment, why not try reading up on this post about ASB vs Unit Trust? You can also learn a thing or two about unit trust first by checking out some of my older articles at the Recommended Read section. Just click HERE.

All in all, I must reiterate the point that I'm not advocating that you should stop investing into ASB. Neither am I bad mouthing ASB and asking your to seek other alternatives instead. Every point made in this post is own my own and backed up with the facts and figures available to me. You be the judge and decide what's good and what's not good for your future.

My final piece of advice for you is to start learning about investing. Stop being ignorant and start empowering yourself with financial education.

Cheers and happy 2016 from Invest Made Easy!

P.S : If you like this post, do:

- Give us a like on our Facebook page

- Give us a "+1" for Google+ located below.

- Spread the knowledge and share this post on Facebook